Gill Capital Partners June 2026 Market Update

As we officially head into summer, we have updates on the historic SpaceX IPO, fundamentals, including inflation, and the possibility of interest rate hikes (yes, hikes) from the Federal Reserve. We are also highlighting Roth IRAs in our “Financial Planning Corner” this month. First, however, we’d like to congratulate the New York Knicks, who brought an NBA championship to New York City for the first time since 1973!

SpaceX IPO

As you’re likely aware, SpaceX completed an Initial Public Offering (IPO) on Friday of last week, raising roughly $75 billion at a valuation of $1.77 trillion, making it the largest IPO on record. As of this writing, SpaceX stock was trading at approximately $200 per share, which equates to a market capitalization of $2.6 trillion. As shown in the graphic below, this catapults SpaceX into the top 5 most valuable public companies in the world, surpassing the value of Microsoft and Amazon for the time being. This is especially remarkable given that SpaceX is not yet profitable.

To put it into perspective, SpaceX’s valuation today is equivalent to 14 Disneys, 5 Costcos, 4 Exxons, or 3 JPMorgans. It is also roughly equivalent to the entire GDPs of Canada and Italy. We would be remiss if we did not mention that SpaceX is the only company on that list that does not generate a profit (yet); in fact, the company lost approximately $4.9 billion in 2025.

Our view

SpaceX is not valued by its current revenue and profit, but for its potential future growth, with investors clamoring to buy its shares. The stock is not trading on fundamentals, but rather the possibility of what SpaceX will become if the company can turn Elon Musk’s dreams into reality. SpaceX is currently trading at roughly 100 times revenue, which is quite stunning. To put that into perspective, NVDA, the world's most valuable public company and darling of the AI boom, trades at roughly 23 times revenue, with astounding revenue growth of nearly 40% per year over the past decade, a feat that is nearly unmatched by any other large company today. SpaceX is already trading at a similar valuation and will need to at least match this type of performance to justify its value today. Can SpaceX live up to the hype? We feel that investors who buy SpaceX should do so with an extremely long time horizon, as this company requires an extraordinary amount of cash to operate and will have to start putting up real growth and profit numbers. If anyone stands a chance, it might be Elon Musk, whose boyish enthusiasm for space travel has energized the investor community.

Update on Economic Fundamentals

Turning to the economy, updated economic reports have been released. Below are recent data points on jobs, wages, and inflation, along with our views on these fundamentals. As a reminder, we focus on fundamentals over headlines, so let's have a look.

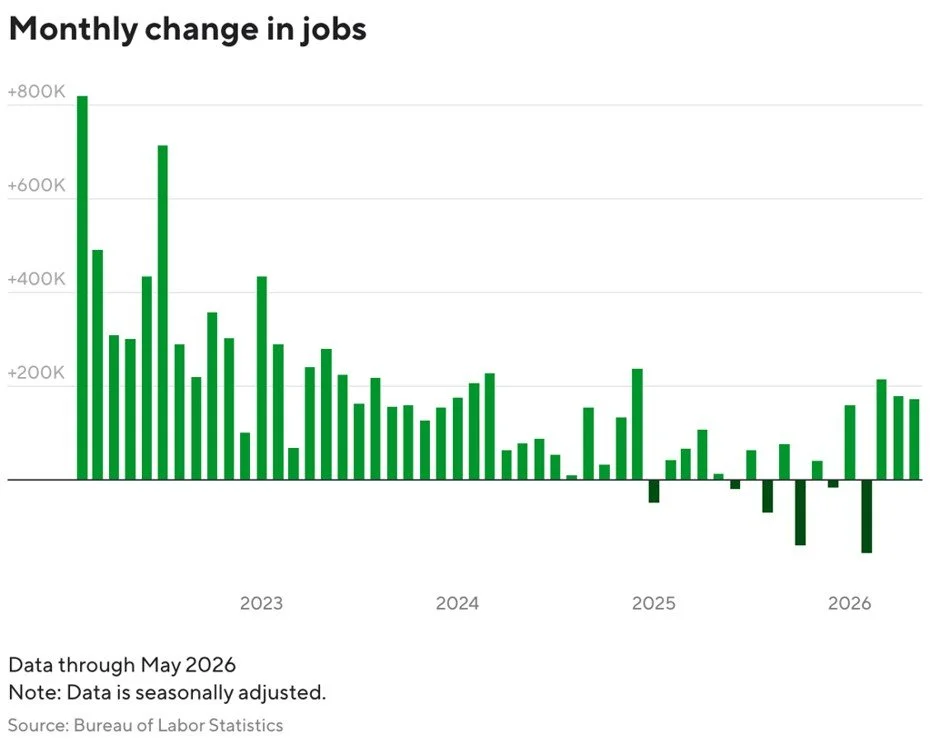

Jobs – Below is a summary of the latest data on the U.S. labor market. As always, we like to look at several sources to provide a comprehensive picture of what is happening in the labor market and what this may mean for the consumer, including reports from ADP, Challenger, Gray & Christmas, and the monthly BLS jobs report (which covers broad employment data, including government employment).

The Bureau of Labor Statistics (BLS) recently released the May jobs report. Total non-farm payroll employment increased by 172,000 jobs, and the unemployment rate held steady at 4.3%. This was better than the estimated 80,000 for the month.

The ADP National Employment Report is a monthly look at private sector employment. In their most recent report, employers reported adding 122,000 jobs in May. This number was modestly above consensus estimates, which expected job growth to be 110,000 for the month.

The Layoff Tracker is a monthly report by Challenger, Gray & Christmas, an executive outplacement and career transition firm that compiles the number of job cuts announced by U.S.-based employers and has been published monthly since the 1990s. The most recent data shows that U.S.-based employers announced 97,006 job cuts in May, up 16% from the month prior, bringing the year-to-date total to 397,755. This is down from the 696,309 announced through the first five months of 2025.

Our view

The jobs picture has stabilized over the past couple of months, with all job reports confirming a more optimistic picture of the labor market compared to the mixed signals and less optimistic trends that we saw in 2025. We continue to see elevated job losses in the technology sector driven by an economy rapidly reshaped by AI; however, in general, the labor market is in fairly good shape due to a lack of labor supply. The big headline in the labor market at the moment is inflation, which continues to pinch consumers. As shown below, with wage growth hovering just above 3.5% and inflation running above 4%, real wage growth is now negative for the first time since 2023, when we were recovering from the COVID-induced inflation bout.

More on inflation below, but the labor market is certainly trending in a more positive direction than we saw last year.

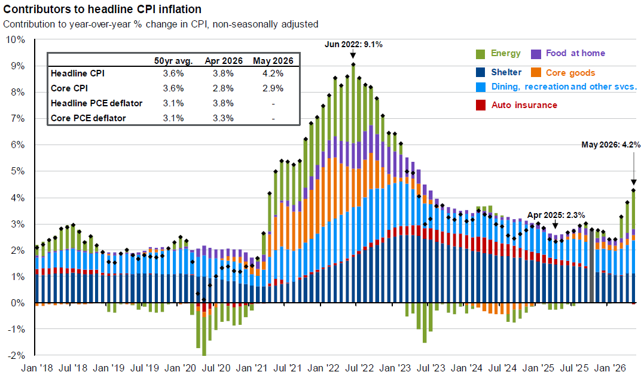

Inflation, Interest Rates & The Federal Reserve – The most recent Consumer Price Index (CPI) report, released by the Bureau of Labor Statistics, shows that prices rose again in May. Headline CPI increased 0.5% month-over-month (seasonally adjusted) in May, and rose 4.2% on a year-over-year basis, well above the Federal Reserve’s 2.0% target. Core CPI, which excludes volatile food and energy prices, rose 0.2% for the month and 2.9% over the past 12 months.

These numbers were generally in line with revised expectations that included impacts from the ongoing war in Iran and surging energy prices.

Our view – Inflation surged past the 4% mark for the first time in three years, largely a result of the spike in energy prices. The market is hopeful this is just temporary and will revert to the more recent trend if a resolution can be reached shortly, reopening oil flows in the Middle East. We are cautiously optimistic that this will be the case, as oil is beginning to come back down; however, we know that the situation is tenuous. Oil futures markets continue to predict lower prices in the not-too-distant future. That being said, inflation remains solidly above the Federal Reserve’s target, and as mentioned above, real wage growth is now negative for the first time in 3 years. This sets up a complicated Federal Reserve handoff for the incoming Federal Reserve Chair Kevin Warsh, who will oversee his first meeting as Fed Chair this week. In reaction to the recent inflation and labor market data, interest rate futures are now pricing in higher rates for longer, with one interest rate increase anticipated near the end of the year. This represents a fairly dramatic about-face, as many were anticipating multiple interest rate cuts in 2026 heading into this year. We are not fully convinced that the Federal Reserve will actually raise interest rates this year, but a protracted wait-and-see approach seems likely. The Federal Reserve is all too aware that this inflationary issue is the result of an oil price shock, which is hopefully temporary, and that higher interest rates really will not do much to mitigate that type of inflation. In the meantime, fixed-income investors can continue to benefit from high interest rates.

Financial Planning Corner

Roth Conversions: Are They Right For You?

The topic of Roth accounts has garnered a lot of attention recently. However, Roth IRAs have been available since the Taxpayer Relief Act of 1997 (which became effective in 1998) and were named after Senator William V. Roth Jr. of Delaware. Roth funds encompass both Roth IRA and Roth 401(k) accounts (available since 2006).

The Roth account allows paying taxes up front, receiving tax-free growth, and paying no additional taxes upon withdrawal. This is in contrast to a traditional IRA, where no taxes are paid up-front, you receive tax-deferred growth, and you pay ordinary income taxes upon withdrawal.

Keep in mind that Roth, pre-tax (traditional), and after-tax (non-retirement brokerage) accounts are all financial tools to keep in your tool belt. You do not need to use every one of these account types in your financial plan; each one has its own benefits and drawbacks.

If your tax bracket is the same prior to retirement and in retirement, the outcomes of pre-tax (traditional IRA) and Roth IRA accumulation and distribution are mathematically identical. However, contributing to Roth IRA accounts or converting traditional IRA accounts to Roth in lower tax years can have significant advantages.

One of the most important considerations for our clients who wish to utilize Roth accounts is related to estate planning. The original SECURE Act (2019) eliminated the Inherited IRA/Stretch IRA over one’s lifetime for most non-spouse beneficiaries. The result was that an IRA account must be depleted within ten years of the account owner’s death. Remember that for traditional (pre-tax) sources of money, either you or your heirs will pay ordinary income taxes upon withdrawal. In contrast, any inherited Roth funds are tax-free, since the taxes have already been paid. Many heirs will receive an inheritance during their peak earning years (in their 50s or 60s), which can compound the issue of paying higher taxes on these account withdrawals.

A Roth conversion can make a lot of sense when the parent is in a lower tax bracket than their children. It is best to pay taxes when they are low, which makes a lot of sense within an intergenerational wealth-planning framework. If there is a low tax year, a shift from full-time to part-time work, a recent retirement, or a period of unemployment, a conversion could make sense. Converting funds from a traditional account to a Roth account can allow them to grow tax-free for several decades, potentially meaningfully reducing the heirs' tax liability.

When discussing Roth conversions with our clients, we ask the following questions:

Will you be converting funds up to the top of your current income bracket or artificially moving yourself into a higher tax bracket?

Are Medicare premiums going to be impacted by the conversion (Income Related Monthly Adjustment Amount – IRMAA), or are you younger than age 63?

Are you in a lower tax bracket currently (due to sabbaticals, the period of time after retirement but prior to claiming Social Security benefits, part-time work, unemployment, or years prior to RMDs)?

How soon will you need to make withdrawals from your accounts, and will you need to access the converted funds in the next few years?

Do you have funds outside of retirement accounts to pay the taxes on the conversion?

How long do you reasonably have for the funds to compound (current age and health)?

Whether or not Roth conversions make sense is determined on an individual basis. Our goal is to help our clients maintain the lowest average tax rates possible over their entire lifetime, not just to minimize their taxes in a single year. While no decision to complete a Roth conversion is absolute (since future tax rates are unknown), having a robust mix of pre-tax, after-tax, and Roth assets can be very useful and provides additional optionality.

We can run detailed Roth conversion analyses in our financial planning software to help you review and discuss your options. Please reach out to your advisor with any questions, and we are happy to speak with you further about utilizing Roth conversions to maximize your financial plan and the legacy you leave to your heirs.

As always, please let us know if you have any questions or concerns, or if we can provide assistance with any other financial planning matters, including education, taxes, insurance, or estate needs.