Gill Capital Partners April 2026 Market Update

Taxes, the Iran war, and a slew of new economic data…April is off to a frenetic start. On a positive note, the D.U. Pioneers Men’s Ice Hockey team defeated the Wisconsin Badgers 2-1 to win their third national championship in five years and eleventh total, the most of any team in collegiate hockey history. Congrats to the Pioneers!

We have a lot to get to. On the economic front, we received multiple data points that provide clues about the economy's trajectory, which come at an interesting time as we begin to see the impact of the war in Iran. We’ll examine interest rates, the Federal Reserve, and how equity markets may be interpreting the conflict and its implications on the global economy.

Before we get into all of this in detail, we are extremely excited to announce our upcoming Speaker Series event featuring Dr. David Kelly, Chief Global Strategist at J.P. Morgan. Dr. Kelly is a renowned figure in economics and markets, and we are thrilled to have him at this exclusive event. Below is some further information on Dr. Kelly, as well as a link to register for the event.

Speaker Series – Dr. David Kelly

Please join us for a private conversation with sought-after industry leader Dr. David Kelly, Chief Global Strategist at J.P. Morgan Asset Management.

Dr. Kelly is one of the most respected and trusted voices in global markets today and is frequently featured on CNBC and Bloomberg, as well as a keynote speaker at conferences worldwide. Dr. David Kelly is the Chief Global Strategist for J.P. Morgan Asset Management. With over 25 years of experience, David provides valuable insight and perspective on the economy and markets to the institutional investor and financial advisor global communities.

Throughout his career, David has developed a unique ability to explain complex economic and market issues in a language that resonates with investors at every level. We are thrilled to have Dr. Kelly present to our clients at such an interesting time for investors.

Iran War Update

While this weekend's U.S.-Iran meeting did not conclude with a final peace agreement, the lengthy meeting did allow the two sides to meet in person and state their positions. With both sides (and the rest of the world) eager to end this conflict, confidence is increasing that the teams will negotiate a resolution that allows both the U.S. and Iran a viable exit. According to Axios, the timeframe to limit or ban nuclear enrichment is a top priority. The U.S. prefers a twenty-year ban, while Iran would like a timeframe in the single digits.

Our view

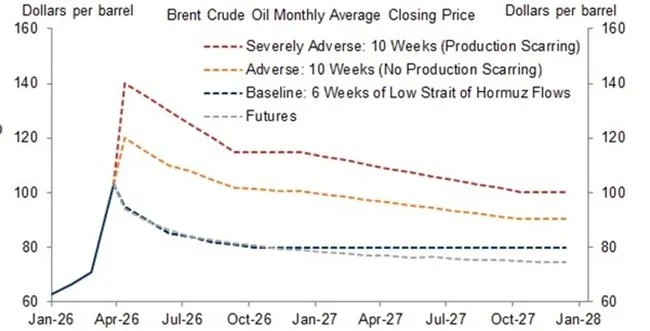

It seems positive that the two sides are talking and bombs are not flying. Perhaps we are getting closer to a resolution? Equity markets certainly think we are, rallying back to near all-time high levels. As of earlier this week, nearly all U.S. equity indexes have erased their losses since the start of the conflict. However, global energy prices remain too high, with little traffic through the Strait of Hormuz. As shown in the chart below, the Goldman Sachs Investment Research team has illustrated various scenarios for oil prices going forward based on the length and severity of the disruption. In their accompanying note, and in light of the recent talks breaking down, they see us currently trending towards the orange line, above their previous baseline scenario.

Any final agreement would require reopening the Strait, but it remains unclear whether it will function as a toll-controlled passage for Iran or return to a free route for global trade. Until a final deal is reached and U.S. ships are on their way home, supply disruptions will persist and commodity markets will remain elevated.

Oil prices are just one of the many issues arising from this conflict, as disruptions to global shipping routes continue to spread quickly. By way of example, product shortages are hitting building product supply chains. The Japanese toilet maker Toto Ltd, which is one of the largest global manufacturers of bathroom fixtures, has suspended new orders due to material shortages caused by the Iran war. “The procurement of raw materials both domestically and internationally has become extremely unstable as a result of the Middle East conflict,” Toto said in a statement released Friday. Japan imports 90% of its crude oil from the Middle East, along with many other chemicals and petrochemicals that are inputs into the manufacturing process. Expect summer disruptions in product availability and higher prices until this is all behind us.

Update on Economic Fundamentals

Turning to the economy, updated economic reports have been released. Below are recent data points on jobs, consumer spending, GDP, corporate earnings, and inflation, along with our views on these fundamentals. As a reminder, we focus on fundamentals over headlines, so let's have a look.

Jobs – Below is a summary of the latest data on the U.S. labor market. As always, we like to look at several sources to provide a comprehensive picture of what is happening in the labor market and what this may mean for the consumer, including reports from ADP, Challenger, Gray & Christmas, and the monthly BLS jobs report (which covers broad employment data, including government employment).

The Bureau of Labor Statistics (BLS) recently released the March jobs report. Total non-farm payroll employment increased by 178,000 jobs, and the unemployment rate held steady at 4.3%, this was better than estimated and marked a reversal from the decline of 133,000 jobs reported the prior month. Including revisions, the three-month average was 68,000 jobs.

The ADP National Employment Report is a monthly look at private sector employment. In their most recent report, employers reported adding 62,000 jobs in March. This number was modestly above consensus estimates, which expected job growth to be near 40,000 for the month.

The Layoff Tracker is a monthly report by Challenger, Gray & Christmas, an executive outplacement and career transition firm that compiles the number of job cuts announced by U.S.-based employers and has been published monthly since the 1990s. The most recent data shows that U.S.-based employers announced 60,620 job cuts in March, bringing the first-quarter total to 217,362, down from the 259,948 jobs lost in the fourth quarter.

Our view

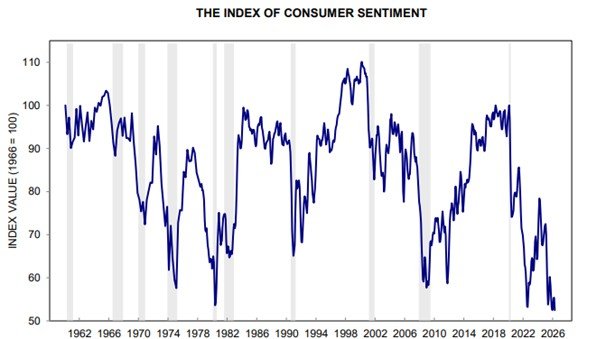

While the jobs picture remains mixed, March data overall points to a late-cycle labor market - one that is still adding jobs, but with weakening breadth. The job market appears to have stabilized a bit for now, with layoffs moderating slightly and new job creation improving slightly, albeit far below historical averages. The big story is that while the labor market is not great, it is fairly stable; however, consumer sentiment just recorded one of its lowest readings on record.

As shown below, the University of Michigan just released its monthly read on consumer sentiment, the first since the Iran war started, and it is not good. In fact, it is the lowest level ever recorded. That being said, consumer sentiment has historically not always been a reliable predictor of actual consumer behavior, though it’s an interesting data point to keep an eye on.

Higher energy prices are driving inflation up, and consumers are feeling the impact. While wage growth is running at 3.5%, inflation just shot up to 3.3%, so it makes sense the consumer is in a foul mood.

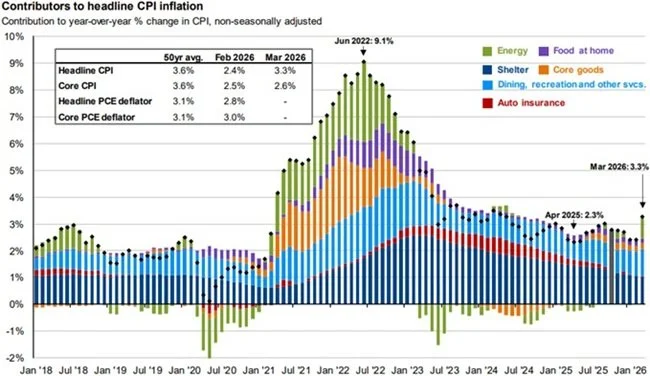

Inflation, Interest Rates & The Federal Reserve – The most recent Consumer Price Index (CPI) report, released by the Bureau of Labor Statistics, shows that prices rose dramatically in March with the onset of the Iran war. Headline CPI increased 0.9% month-over-month (seasonally adjusted) in March, and rose 3.3% on a year-over-year basis, well above the Federal Reserve’s 2.0% target. Core CPI, which excludes volatile food and energy prices, rose 0.2% for the month and 2.6% over the past 12 months.

Interest rates initially spiked in the early days of the war and have now stabilized, albeit at higher levels than before the war. The sharp re-acceleration in headline inflation is likely to delay any Federal Reserve rate cuts for some time, until there is more clarity on the situation.

Our view – Just when we were hoping that inflation was coming under control, we get a massive war-induced supply shock. As of now, the Fed is in wait-and-see mode, and it is likely to remain there until this war is resolved or it causes a major economic slowdown.

As we have been discussing in our Investment Committee recently, oil shocks have a long track record of preceding periods of economic weakness. Many forget that the 2008-09 “Great Recession” was actually initiated by a spike in oil that sent prices up to nearly $150/barrel, massively slowing the global economy and eventually uncovering all of the financial issues that ultimately brought the global financial system to its knees.

Recently, we have seen oil prices spike to $120/barrel, and as of this writing, they are around $95/barrel. While we are all too familiar with the history of oil price spikes and recessions, there are a few key differences. First, the price of oil at $150/barrel right before the Great Recession, inflation-adjusted for today’s dollars, would be over $200/barrel. While prices are high, they are nowhere near what they were then on an inflation-adjusted basis. Furthermore, forward oil curves are projecting lower prices in the future, also known as “backwardation,” which signals acute short-term supply tightness but no real concern of a lasting shortage. Equity markets are also likely trading on the belief that this is relatively short-lived.

As always, please let us know if you have any questions or concerns, or if we can provide assistance with any other financial planning matters, including education, taxes, insurance, or estate needs.