Gill Capital Partners Thanksgiving 2025 Market Update

We would like to express our sincere gratitude to all of our clients, partners, friends, and colleagues. We sincerely hope that you have a peaceful and enjoyable Thanksgiving.

The past month has seen several key developments, including the end of the government shutdown, which caused a significant delay in key economic reports. As a result, we do not have all of the economic data we’re accustomed to having at month-end, but we will review what we have. We will also examine recent developments at the Federal Reserve to glean clues about where interest rates may be headed in the near term. Finally, we will review IRS updates to 2026 tax brackets, standard deductions, and other changes for 2026. Before we get into all of that, however, we wanted to share that the penny is being discontinued. What does this mean?

In February of this year, President Trump ordered the U.S. Treasury Department to stop minting pennies, as they cost more to produce than they are worth. The U.S. Mint said in its annual report that each penny now costs 3.69 cents to make. Pennies are not going away, as there are still approximately 250 billion pennies in circulation. However, their circulation will continue to slow as many of the Federal Reserve coin terminal facilities, which circulate coins, are no longer taking or distributing pennies. Pennies do remain legal tender. The nickel may be next, as each nickel costs roughly 13 cents to produce.

Update on Economic Fundamentals

Turning to the limited recent economic reports that have been released, below are recent data points on jobs, consumer spending, inflation, and the Federal Reserve, as well as our views on the fundamentals.

Jobs & Consumer Spending – Below is a summary of the most recent data points on the U.S. labor market. As always, and particularly now with the lack of governmental data, we like to look at several sources to provide a comprehensive picture of what is happening in the labor market and what this may mean for the consumer, including reports from ADP, Challenger, Gray & Christmas, and the monthly BLS jobs report (which covers broad employment data, including government employment).

The BLS released the September jobs report last week. It was originally scheduled for release on October 3rd; however, due to the Federal Government shutdown, it was released on November 20th. The October jobs report, which was scheduled to be released in early November, will not be released. The BLS has announced that it will not publish this report because the “household survey” data could not be collected during the federal government shutdown. The delayed September report, as released by the BLS, showed that the U.S. economy added 119,000 jobs in September, which was above market expectations of around 50,000 jobs, and the unemployment rate held steady at 4.4%. The prior month revisions for July and August revised job growth lower by approximately 33,000 jobs combined over the two months.

The ADP National Employment Report is a monthly look at private sector employment, and they published data for the month of October. Private employers reported that hiring increased by 42,000 jobs in October. This number was modestly better than consensus estimates, which were expecting to see job growth near 25,000 for the month.

The Layoff Tracker is a monthly report by Challenger, Gray & Christmas, an executive outplacement and career transition firm, that compiles the number of job cuts announced by U.S.-based employers and has been published monthly since the 1990s. Employers announced 153,074 job cuts in October 2025, a 183% increase from the previous month. Total year-to-date layoffs now stand at 1,099,500, representing a 65% increase from the comparable period last year, marking the highest number through August since 2020.

U.S. retail sales slowed in September, per the delayed report by the Census Bureau. Headline sales climbed just 0.2% in September, below economists' expectations of 0.4%. By comparison, sales rose by 0.6% in August.

Our view

Given the interruption in Federal government reporting, we need to rely more heavily on private sector data, along with other relevant data, to provide a clearer picture of what is happening in the labor market. The data shown above, taken together, provides a clear picture of a weakening labor market, one that has likely shifted from being very tight from an employer's perspective to softer and more normal from a historical perspective. Furthermore, alternative labor market data points, including job openings, quits, and layoffs over the past few months, clearly indicate a softening labor market, albeit one that may be transitioning to less restrictive and competitive levels for employers compared to the post-COVID period.

So, how is the consumer holding up, given a weakening labor market? While the labor market has weakened and unemployment has risen to 4.4%, the current unemployment rate remains significantly lower than the 50-year average of 6.3%. For the moment, wage growth, which was recently reported at 3.8%, just barely above the current inflation rate of 3.0%, continues to support household spending, but retailers report that consumers are becoming more selective with their purchasing. The holiday season is upon us, marking the most important time of year for retailers. We will be closely monitoring these spending reports for clues on the health of the consumer during this period. Finally, consumer sentiment, as shown below, is near all-time low levels, likely representing the broader geopolitical backdrop, but shows broader evidence of a potentially softer consumer market.

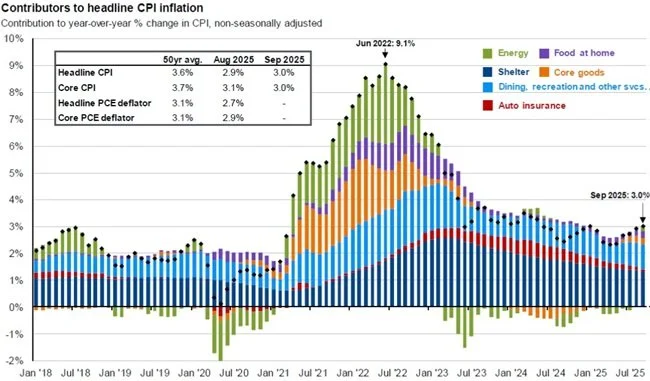

Inflation – Like job reports, inflation reports have also been delayed, and it is unclear whether the October data will be released at all. The last report released was the monthly Consumer Price Index (CPI) for September, which showed that prices accelerated 3.0% from the same month a year ago and 0.3% for the month. Core CPI, which excludes food and energy prices, increased 0.2% for the month and 3.1% from a year ago. While these numbers were slightly better than the market was anticipating, they remain above the Fed’s target inflation rate of 2.0%, and the near-term trend appears to be moving in the wrong direction.

Our view – Unfortunately, inflation data has become a highly politicized data point. It is an important input into the Federal Reserve’s decision-making process, and the lack of timely data comes at a critical time as the Federal Reserve is wrestling with dual mandates that appear to be moving in opposite directions. Consumer prices increased in September, as shown in the chart above, and we may never receive October data. This was the fifth consecutive monthly increase and remains above the Federal Reserve’s target of 2%. The data continues to put monetary policy experts in a very difficult spot as they wrestle with labor market weakness and inflation that remains above their long-term target.

Interest Rates & The Federal Reserve - At its October 2025 meeting, the Federal Reserve cut its target federal funds rate by 25 basis points (0.25%), bringing the range down to 3.75%-4.00%. The 10-2 decision in favor of the cut was not unanimous: one member, Stephen Miran, who was recently appointed by President Trump, again dissented, preferring a larger 50-basis-point cut, while Jefferey Schmid favored no change to the target rate.

An update of policy projections, also known as the “Dot Plot,” suggests additional rate cuts through 2025, with the projected federal funds rate at approximately 3.5% -3.75% by the end of the year, and falling further to 3.25%-3.5% by the end of 2026.

Our view

The Fed currently finds itself in a very difficult position, with its two mandates (maintaining stable prices and full employment) appearing to be moving in opposite directions. This is further complicated by the missing data resulting from the government shutdown. The Fed has expressed real concern that missing or delayed data could potentially delay further cuts. As they sit today, Fed Funds futures show an 80% probability of another quarter-point cut at the next meeting on December 10th. They likely will not have more inflation data by then, so it will be extremely interesting to see what they do. We will be watching closely, and the markets are laser-focused on any data coming out that could provide clues as to what the Fed might do next.

IRS Annual Inflation Updates – The IRS recently published the last of the annual inflation updates for 2026. This includes updates to tax brackets, standardized deductions, and retirement account contribution limits, among other items. Below are a few key updates for 2026.

2026 IRA Contribution Limits - $7,500. The catch-up contribution limit for individuals aged 50 and older increases to $1,100.

2026 401(k), 403(b), 457(b) contribution limits – The salary deferral limit for 401(k) and other similar plans is increased $1,000 to $24,500. The catch-up contribution limit for 401(k) and other similar plans for individuals aged 50 and above increases by $500 to $8,000. The so-called “super catch-up” for people who turn 60,61,62, or 63 remains at $11,250.

For 2026, the maximum HSA contribution for somebody with self-only coverage under a high-deductible health plan is $4,400. The limit for somebody with family coverage under such a plan is $8,750.

These are standard inflation-based changes that the IRS makes most years. If you have questions about how any of these changes impact you directly, don’t hesitate to reach out.

The end of the year is sure to be intriguing from an economic perspective. From everyone at Gill Capital Partners, we wish you a very happy Thanksgiving!

As always, please let us know if you have any questions or concerns, or if we can provide assistance with any other financial planning matters, including education, taxes, insurance, or estate needs.