Gill Capital Partners February 2026 Market Update

February is quickly coming to a close, and it was a busy one in the world of economics and markets. On the economic front, we received multiple data points that provided clues into the trajectory of the economy. Additionally, the Supreme Court struck down most of the Trump administration's tariffs, sending ripples through global markets. We will take a look at interest rates and the Federal Reserve following the release of recent economic data. We continue to track international and emerging market stocks, which are outperforming their U.S. counterparts, while crypto assets like Bitcoin are experiencing their worst month since June 2022. We will get into all of this in detail, but before we do, what in the world is going on with software and technology stocks this year?

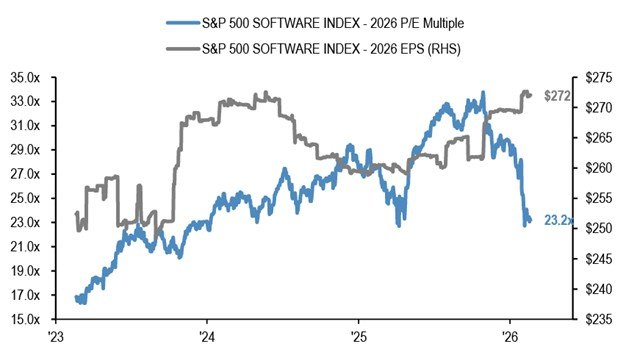

As shown in the chart below, the S&P 500 Software Index has lost over 1/3 of its value in the last couple of months despite strong earnings. This decline includes names such as Microsoft, Adobe, Salesforce, and others. Investors have grown increasingly worried that advanced AI tools could replace existing enterprise software, and subscription-based SaaS models that rely on “seat counts” look less secure as investors start to price in the impact of AI on jobs.

Microsoft, for example, is down nearly 30% from its November peak. Microsoft’s recent earnings report was very strong, with both revenue and earnings beating expectations, up 17% and 24% respectively over last year. Yet the stock has been moving consistently lower for the reasons outlined above. Microsoft is currently trading at a P/E ratio of 24, about the same as Exxon, which has seen year-over-year earnings growth decline. Does this represent a great buying opportunity for software stocks or has the market accurately projected the future impact of AI?

Update on Economic Fundamentals

Turning to the economy, updated economic reports have been released. Below are recent data points on jobs, consumer spending, GDP, corporate earnings, and inflation, along with our views on these fundamentals. As a reminder, we focus on fundamentals over headlines, so let's have a look.

Jobs– Below is a summary of the latest data on the U.S. labor market. As always, we like to look at several sources to provide a comprehensive picture of what is happening in the labor market and what this may mean for the consumer, including reports from ADP, Challenger, Gray & Christmas, and the monthly BLS jobs report (which covers broad employment data, including government employment).

The Bureau of Labor Statistics (BLS) recently released the December jobs report. Total non-farm payroll employment increased modestly by 130,000 jobs and the unemployment rate held steady at 4.3%, this was better than the estimate of 55,000 jobs for the month. This month’s report also incorporated the annual revisions. Those revisions lowered the initial counts by a total of 898,000 jobs, showing that 2025 was much weaker than initially reported.

The ADP National Employment Report is a monthly look at private sector employment. In their most recent report, employers reported that hiring increased by 22,000 jobs in January. This number was modestly below consensus estimates, which expected job growth to be near 25,000 for the month. Private sector jobs have also seen a meaningful slowdown from the pace of the last couple of years.

The Layoff Tracker is a monthly report by Challenger, Gray & Christmas, an executive outplacement and career transition firm that compiles the number of job cuts announced by U.S.-based employers, and has been published monthly since the 1990s. The most recent data shows the U.S.-based employers announced 108,435 job cuts in January, the highest since January 2009.

Our view

There is a lot of noise in the most recent data, largely due to the annual revisions. The annual benchmark revisions occur each year and provide true-ups where estimates were used throughout the year. For 2025, we saw significant downward revisions. 2025 was already reported to show below-average job creation. The revisions imply a much slower pace of job growth than was previously reported, with only 584,000 jobs created in 2025. This compares to over 2 million jobs created in 2024, and the long-term average of 1.5 million jobs per year. Hiring is soft, but overall unemployment remains relatively low, providing a mixed labor picture at the moment.

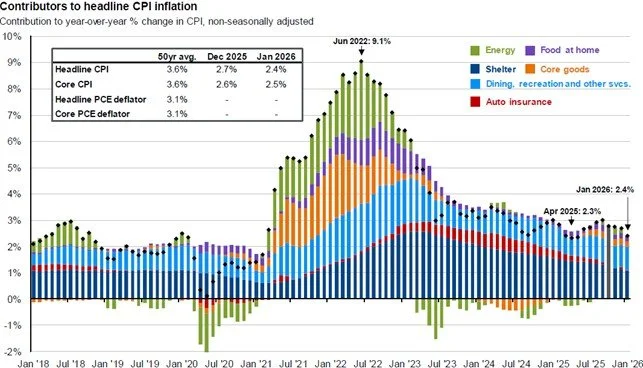

Inflation, Interest Rates & The Federal Reserve – The most recent Consumer Price Index (CPI) report, released by the Bureau of Labor Statistics, shows that prices continued to rise in January, albeit at a slightly slower pace. Headline CPI increased 0.2% month-over-month (seasonally adjusted) in January, and rose 2.4% on a year-over-year basis, down modestly from prior months and slightly below analyst expectations, but still above the Federal Reserve’s 2.0% target. Core CPI, which excludes volatile food and energy prices, also rose 0.3% for the month and 2.5% over the past 12 months. Shelter and food costs were among the largest contributors to monthly inflation, while energy prices eased, helping push the index lower.

Interest rates have drifted modestly lower over the past month following the most recent inflation and labor data. Interest rate futures have been largely unchanged over the past month, with the market anticipating two quarter-point rate cuts by the end of 2026.

Our view – While inflation was modestly better than expectations last month, and is moving in the right direction, the trend of the past few months is largely flat and remains stubbornly above the Fed’s targets. Energy prices, led by lower oil and gas prices in January, are sharply higher in February due to the risk of conflict with Iran. This may drive a retracement higher in the months to come if prices remain elevated.

There was no Federal Open Market Committee meeting in February, and interest rate expectations remained largely unchanged, with rates drifting modestly lower throughout the month. The dramatic Supreme Court ruling, which found the Trump Administration's tariff policy largely illegal, particularly the announcement of new blanket global tariffs, has introduced new uncertainty into markets that had just come to terms with the prior tariff announcements. This will likely extend the Federal Reserve’s wait-and-see policy, as it will now need to ascertain the impact of the new tariff policy.

Corporate Earnings – We are reaching the tail end of earnings season, and with 451 out of 500 companies in the S&P 500 having reported Q4 2025 earnings, we can get a pretty good look at corporate earnings. Of the companies that have reported, 82% beat their sales estimates, with aggregate sales growth of 8.84%, and 72% beat their earnings expectations, with earnings growth of 11.77%. Revenue growth for the year is just over 9%, marking a solid year of corporate sales growth. Forward-looking guidance remains strong, with consensus estimates projecting roughly 15% earnings growth in 2026.

Our view – We get a lot of questions about what is driving stocks higher in the current environment, and why stocks aren’t reacting more negatively to macro & geopolitical headlines. We believe that the answer lies largely with corporate earnings. At the end of the day corporate earnings remain robust. Consumer and corporate spending continue to drive increased corporate sales, while cost controls and anticipation of AI-induced efficiency are expanding corporate earnings.

Tariff Policy – The Supreme Court on Friday struck down a huge chunk of President Donald Trump’s tariff agenda, delivering a major rebuke of the president’s key economic policy. The ruling is a massive loss for Trump, who has made tariffs a central feature of his second presidential term. The decision noted that in order to justify the “extraordinary” tariff powers, Trump must “point to clear congressional authorization. He cannot.” The ruling was silent on whether tariffs paid at the higher rates will need to be refunded. That sum could total $175 billion, according to a new estimate from the Penn Wharton Budget Model. Trump’s legal stance “would represent a transformative expansion of the President’s authority over tariff policy,” the majority concluded. They highlighted that Trump imposed the tariffs without Congress, which has the power to tax under the Constitution. In response to the decision, President Trump immediately announced a new executive order imposing a 10% “global tariff” under Section 122 of the Trade Act of 1974, and the following day increased it to 15%.

Our view – The eventual resolution of tariff policy and the question of refunds is sure to take months, if not years, to clarify, and we see the Supreme Court decision and the Trump Administration's subsequent reaction creating uncertainty. Businesses and government need to know what the playing field looks like in order to develop policy and create plans. This uncertainty around tariffs will potentially slow business investment and decision-making. We will continue to follow this as it unfolds and will provide future updates as they are relevant.

As always, please let us know if you have any questions or concerns, or if we can provide assistance with any other financial planning matters, including education, taxes, insurance, or estate needs.